Since voters in the United Kingdom decided to leave the European Union last week, US consumers, investors and even travelers are trying to understand the impact of the historic Brexit vote. The question I continue to field is" “What does Brexit mean for MY money?” Unlike the run of the mill correction that we saw earlier this year, the UK’s exit from the 28-member union is an “exogenous event.” That means that it has come from outside the predicted modeling system that most economists utilize and as a result, can have significant, negative effects on prices.

For example, the British pound sterling tumbled to its lowest level against the US dollar in thirty years and global stocks have fallen sharply. Meanwhile, bastions of safety like US treasuries, German bunds and gold are rising. Still, large financial firms are saying that so far, there is no liquidity crisis and markets are functioning well.

While that is indeed good news, let’s not repeat old mistakes. Consider this: nine years ago this month, June, 2007, an unexpected event occurred: investment banking firm Bear Sterns (BS) had to bail out two of its hedge funds that were collapsing because of bad bets on subprime mortgages. At the time, there was no mystery surrounding the risks that were emerging, though 15 months later, there were complaints that the financial media had failed to sound the warning alarms.

In fact, the New York Times said the crisis at BS stemmed “directly from the slumping housing market and the fallout from loose lending practices that showered money on people with weak, or subprime, credit, leaving many of them struggling to stay in their homes. Bear Sterns averted a meltdown this time, but if delinquencies and defaults on subprime loans surge, Wall Street firms, hedge funds and pension funds could be left holding billions of dollars in bonds and securities backed by loans that are quickly losing their value.”

Let’s put that seemingly small BS event from nine years ago into context:

- June 2007: BS Bails out funds

- October 2007: US stock indexes hit all-time highs

- March 2008: BS goes broke and is taken over by JP Morgan Chase

- September 2008: Lehman Brothers Holdings files for Chapter 11 bankruptcy protection; Bank of America purchases Merrill Lynch; the Federal Reserve Bank of New York is authorized to lend up to $85 billion to AIG; the Reserve Primary Money Fund falls below $1 per share; Goldman Sachs and Morgan Stanley become bank holding companies

I am not suggesting that Brexit will cause a financial crisis, but we should carefully consider what dangerous spillover effects could occur. While US banks are better capitalized than they were leading up to the fall of 2008, the UK and European banks do not look nearly as healthy. In the two trading sessions after Brexit, the European Bank index lost about a quarter of its value and UK based banks did even worse.

If you are traveling to the UK or Europe or you enjoy imported cheese and wine, you might be delighted to see the US dollar strengthen. But as the dollar rises, emerging markets like China could come under pressure, echoing what happened in the first six weeks of the year, when global stocks tumbled and US stock corrected. And if European growth slows, its weaker economies (Portugal, Italy, Greece, Spain) will once again be at the heart of sovereign debt questions.

In terms of the US, analysts at Capital Economics say the UK and the EU account for 4 and 15 percent of US exports, respectively. If both regions go into a recession, Brexit could shave 0.2-0.3 percent from the current US growth rate of 2 percent. But estimates can be rocked by emotions. A US-based multinational may hold back on hiring everywhere to see how things shake out post-Brexit. For US exporters, the rising US dollar will create a drag on competitiveness in overseas markets and could potentially trigger lay offs at home. And if non-affected businesses and consumers start to feel unnerved, they too might pull in the reins, causing the US economy to slow down more than anticipated.

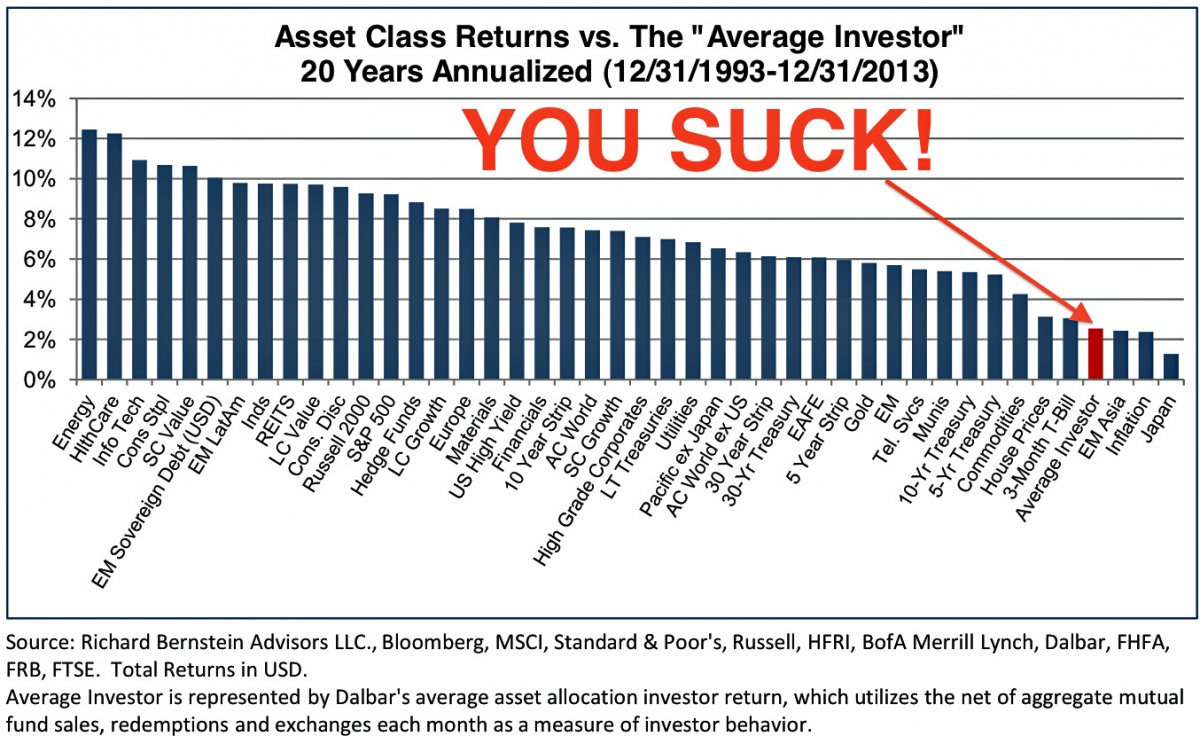

Amid all of this uncertainty, anxiety levels are rising, testing the third longest bull market in history. Some may feel butterflies and may even be tempted to sell. Remember that market timing rarely works because even if you sell and manage to steer clear of the bear by staying in cash, you will not be able to reinvest dividends and fixed-income payments at the bottom and you are likely to miss the eventual market recovery. There is clear evidence that when investors react either to the upside or downside, they generally make the wrong decision.

The best way to avoid falling into the trap of letting your emotions dictate your investment decisions is to remember that you are a long-term investor and do not have all of your eggs in one basket. Your diversified portfolio strategy, based on your goals, risk tolerance and time horizon should help you fight the urge to react to short-term market conditions. It’s not easy to do, but sometimes the best action is NO ACTION. And don’t forget that if you are still contributing to your retirement plan or funding your kid’s education fund, take comfort in knowing that you are buying shares at cheaper prices.

If you are really freaked out about the movement in your portfolio, perhaps you came into this period with too much risk. If that’s the case, you may need to trim readjust your allocation. If you do make changes, be careful NOT to jump back into those riskier holdings after markets stabilize. Finally, if you need access to your money in the short-term (within the next 6-12 months), be sure that it is not invested in an asset that can fluctuate.

![Jill on Money [ Archive]](http://images.squarespace-cdn.com/content/v1/59efbd48d7bdce7ee2a7d0c4/1510342916024-TI455WZNZ88VUH2XYCA6/JOM+Blue+and+White.png?format=1500w)